Editors’ Note: This article covers a micro-cap stock. Please be aware of the risks associated with these stocks.

The most likely result of drilling a “wildcat” exploration well is a dry hole. As I understand it the odds of success on an exploration well are something like one or two in ten if the well is being drilled in an area reasonably prospective for hydrocarbons.

The odds aren’t great. But the rewards often are.

My portfolio is focused on unconventional oil producers that are developing shale or tight oil reservoirs in North America. I like the unconventional producers because these companies don’t take exploration risk. These companies are drilling into defined resource plays and know they are going to find oil when they drill a well.

While these unconventional producers don’t have exploration risk, there are a couple of things that aren’t as attractive about them:

– Unconventional wells are not very prolific and decline rapidly which means that they offer only reasonable rates of return

– Without high oil prices ($85 plus) these wells don’t make much money at all

I liken unconventional development to a baseball player who consistently hits singles. The unconventional wells aren’t going to make a lot of money quickly, but over time the results are very satisfying.

“Wildcat” conventional exploration drilling is more like a homerun hitter. While the homerun hitter strikes out a lot the reward for exploration success can be many multiples of the cost of the well.

For a small company one big exploration success can result in multi-bagger returns for shareholders.

As with every year there are a few exploration wells being drilled in 2013 that could be “company makers”.

African Hydrocarbons (KNPRF.PK) – Exploration in Tunisia

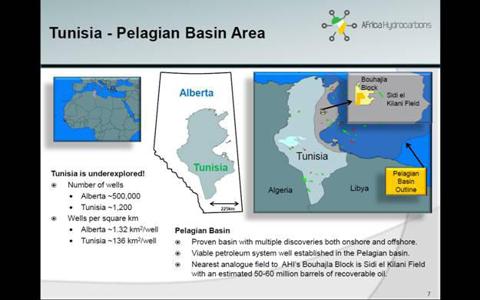

North African country Tunisia is one of the few remaining underexplored onshore regions in the world. For some perspective on how underexplored Tunisia is we can compare it to the Canadian province of Alberta. While the province of Alberta in Canada has had 500,000 wells drilled, Tunisia has had only 1,200.

It is pretty common knowledge that there are no large new conventional oil pools waiting to be discovered in Alberta. All of that easy fruit has been picked. Tunisia meanwhile still offers potential for massive conventional discoveries.

Tunisia is starting to get some more attention. One of the more noteworthy moves into Tunisia is being made by Shell (RDS.A). In 2013 Shell is planning to drill four exploration wells that will cost a combined $150 million.

If Shell finds something large in Tunisia it isn’t going to move the needle for a company of that size. The adventurous side of me has me more interested in companies that have more leverage to one large exploration success.

Canadian listed African Hydrocarbons is a pure play on Tunisia. The company has the potential to make investors multiples of their investment from the current share price should the current ongoing exploration program result in success.

African Hydrocarbons partner Dualex (DALXF.PK) is currently preparing to drill its 3D seismic defined BNH-1 location on its Bouhajla North prospect in Tunisia. This prospect is the mirror image of the nearby (25 kilometers away) Sidi el Kilani field that has produced 50 million barrels of oil from only five wells.

Compare Sidi el Kilani to the North American tight oil plays that we are developing today which might require more like 200 wells to recover 50 million barrels instead of 5 (assuming 250,000 barrels per well).

You can see pretty easily why a large conventional vertically produced field is so much more profitable than resource play development. Five wells cost a lot less to drill than 200.

The BNH-1 well could hold a reservoir similar to the 40 to 50 million barrels of oil that Sidi el Kilani has. Africa Hydrocarbons has a 47.5% working interest in BNH-1.

In addition to Bouhajla North, African Hydrocarbons actually has two larger but less well defined prospects on the acreage (Bouhajla Northeast and Bouhajla Southeast). Both of these additional prospects are huge but require additional seismic work.

With the Sidi el Kilani producing field nearby there is plenty of infrastructure already in place, so even a modest discovery could be very profitable for African Hydrocarbons. Ideally the African Hydrocarbons team would like the BNH-1 well to result in a large discovery. But if it is something more modest the well could be turned into a cash flow engine to provide the funds to finance drilling of the next two wells on the block.

As far as geo-political risk goes Tunisia is obviously not Alberta. But for a country situated in North Africa it is actually a pretty reliable place for foreign companies to operate. Nevertheless this is a volatile region of the world which is another risk to consider.

African Hydrocarbons is a pretty simple story. If BNH-1 hits on something similar to Sidi el Kilani then this stock is a multi-bagger for shareholders immediately. If BNH-1 is a dry hole then the company is likely going to have to do some creative financing to fund its next exploration well.

That is the fun of the old school “wildcat” business model. It is high risk and high reward.

WesternZagros (WZGRF.PK)

There is Kurdistan, one last great onshore oil exploration frontier where finding a billion barrels of oil in a low cost easy to produce conventional reservoir is a real possibility.

Last week in a very controversial move, the Turkish state run oil firm struck a deal with Iraq’s semi-autonomous Kurds and Exxon Mobil (XOM) to develop projects in Northern Iraq.

The Government in Iraq thinks such a deal is illegal and the Government of the United States doesn’t support it. This is a sensitive issue in a volatile part of the world.

What the deal is going to do is give that oil developed in Kurdistan a direct route out of Iraq and into the world market. That could make oil found in the region much more valuable in the near term.

It also is another signal that Exxon is planning to be a big presence and settle in for a long term stay in Kurdistan. And that has to be good news for neighboring independent producers which have already made big discoveries in the region and have additional high impact exploration wells to drill.

WesternZagros is one such neighboring company in Kurdistan. WesternZagros inked its first Kurdistan contract way back in 2004. The company holds a 40% working interest in two valuable Production Sharing Contracts.

The first contract is on the block called Garmian where WesternZagros is partners with Gazprom (GZPFY.PK) (40%) and Government of Kurdistan (20%). The second contract is on the block called Kurdamir where WesternZagros is partners with Talisman (TLM) (40%) and the Government of Kurdistan (20%).

On the Kurdamir block WesternZagros already has a giant oil discovery. The Kudamir-1 and Kurdamir-2 exploration wells have identified almost 1 billion contingent barrels of oil.

Discoveries like that can’t be made in North America these days.

There is a saying in the oil industry that “big oil fields tend to get bigger over time”. That is why I’m watching the upcoming Kurdamir-3 well which is being drilled in 2013 and could significantly further increase the estimates of oil in place.

Kurdamir-3 was spud on February 25 and is expect to take four months to drill. The well is being drilled on the southwest flank of the Kurdamir structure, around 3 km and 5 km from its Kurdamir-1 and Kurdamir-2 discovery wells, respectively.

This well is testing the potential for another 200 to 250 million contingent barrels of oil in place. If successful that is another step change in value for WesternZagros shareholders and would have to put the company in the sights of Exxon who has the means to efficiently develop discoveries of this size.

The Garmian block also has had a successful discovery with the Sarqala-1 well which has produced over 1 million barrels of oil since starting production in October 2011. There are several follow up exploration wells planned for this block.

WesternZagros has already found a lot of oil, but the company has only drilled four wells and is still really just getting started in Kurdistan. In total the company is chasing exploration targets that are in total prospective for 4.7 billion barrels of oil equivalent.

Kurdamir-3 is the next big potential catalyst for this company hunting elephant sized discoveries.

Seeking Alpha

You must be logged in to post a comment.